The American middle class is facing one of its toughest financial periods in decades. Millions of hardworking families who once believed stable jobs and regular paychecks would provide financial security are now struggling to keep up with rising expenses, growing debt, and economic uncertainty. In 2026, many middle-class Americans say they feel financially exhausted despite working harder than ever before.

The problem is not limited to low-income households anymore. Teachers, office workers, nurses, truck drivers, small business owners, and even dual-income families are increasingly living paycheck to paycheck. From housing and healthcare to groceries and insurance, nearly every major expense category has become more expensive over the past few years. Financial experts warn that the middle class is being squeezed from every direction at once.

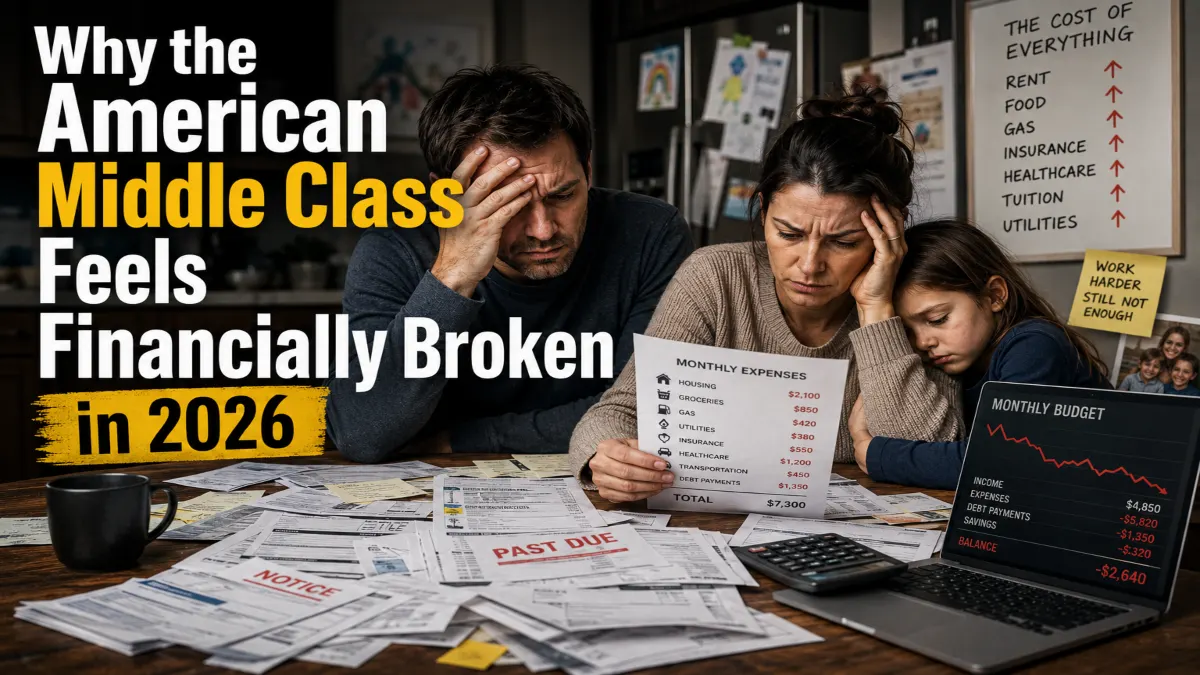

Rising Costs Are Outpacing Paychecks

One of the biggest reasons middle-class Americans feel financially trapped is the growing gap between wages and living expenses. While incomes have increased in some industries, everyday costs have risen much faster for many households.

Groceries continue to consume a large share of family budgets. Basic household essentials that once felt affordable now cost significantly more than they did just a few years ago. Many families are shocked at how quickly grocery bills climb during routine shopping trips.

Housing expenses remain another major pressure point. Rent prices are still elevated across many cities, while high mortgage rates have made homeownership difficult for first-time buyers. Families that already own homes are dealing with rising property taxes, maintenance costs, and homeowners insurance premiums.

Transportation costs are also creating problems. Americans are spending more on:

- Gasoline

- Car insurance

- Vehicle maintenance

- Auto loan payments

- Public transportation

Healthcare costs continue to rise as well. Insurance premiums, prescription prices, and medical bills are making it harder for families to save money or pay down debt.

Even households with decent salaries are struggling because their expenses keep increasing faster than their income.

Credit Card Debt Is Becoming a Lifeline

Many middle-class Americans are relying heavily on credit cards just to maintain normal lifestyles in 2026. Credit cards are no longer being used mainly for luxury purchases or vacations. Instead, families are increasingly using them for necessities like groceries, fuel, utility bills, and emergency expenses.

The problem becomes even worse because interest rates remain extremely high. Americans carrying balances are paying massive amounts in interest charges every month, making it difficult to reduce debt.

Recent financial reports show U.S. credit card debt has reached record levels, with many consumers carrying balances they cannot fully repay.

Financial experts say this creates a dangerous cycle:

- Rising expenses increase credit card use

- Interest charges make balances grow faster

- Debt payments reduce available income

- Savings become harder to build

For many families, this cycle has become a permanent part of everyday financial life.

Emergency Savings Are Quickly Disappearing

One of the biggest signs of financial stress among the middle class is the shrinking amount of emergency savings available to households.

Financial advisors traditionally recommend saving three to six months of living expenses for emergencies. However, many Americans in 2026 are far below that target.

Unexpected expenses such as medical emergencies, car repairs, or home maintenance problems are forcing families deeper into debt. Instead of using savings accounts, many households are relying on credit cards or personal loans to survive financial emergencies.

Economic uncertainty is making the situation even more stressful. Workers worry about layoffs, reduced work hours, or economic slowdowns because they know they may not have enough savings to handle sudden financial disruptions.

Many Americans report feeling one major emergency away from serious financial trouble.

Housing Is Consuming Too Much Income

Housing has become one of the largest financial burdens facing middle-class Americans. Rent and mortgage payments are consuming a growing share of monthly income, leaving less money available for savings, retirement, or family expenses.

High mortgage rates have created enormous challenges for homebuyers. Even families with stable incomes are finding it difficult to afford monthly payments on modest homes.

Renters are also struggling. In many cities, rental prices have remained elevated despite slower inflation overall. Families are being forced to spend larger portions of their paychecks simply to secure housing.

As housing costs rise, Americans are delaying major life decisions such as:

- Buying homes

- Starting families

- Having additional children

- Relocating for better opportunities

- Saving for retirement

Financial experts say the housing affordability crisis is one of the biggest reasons middle-class families feel financially unstable in 2026.

Americans Are Working More but Saving Less

Despite financial pressure, many Americans are working harder than ever before. Side hustles, freelance jobs, online businesses, and gig work have become increasingly common as households search for additional income.

Many workers now juggle multiple jobs simply to cover rising living expenses. Some drive for delivery services after regular work hours, while others take weekend jobs or freelance projects to supplement income.

However, earning more money has not necessarily improved financial stability for many households. Higher living costs often absorb extra income almost immediately.

Financial experts say many middle-class Americans are experiencing “income fatigue,” where people continue working more but still feel financially stuck.

This constant pressure is creating emotional exhaustion and frustration among workers who believed financial security would improve with career growth.

Younger Families Face a Different Economic Reality

Millennials and Gen Z families are experiencing financial challenges that differ significantly from previous generations. Many younger Americans entered adulthood during periods of inflation, rising housing costs, and economic instability.

Student loan debt remains a major burden for millions of younger workers. At the same time, expensive housing markets are making it harder to buy homes or build wealth.

Younger families are also dealing with expensive childcare costs, healthcare expenses, and rising insurance premiums. Many parents say raising children feels significantly more expensive than expected.

As a result, younger Americans are delaying important financial milestones, including:

- Homeownership

- Marriage

- Retirement investing

- Family expansion

- Career changes

Many younger workers also worry they may never achieve the same level of financial stability their parents once had.

Retirement Feels Increasingly Uncertain

Retirement planning has become another major source of anxiety for the American middle class. Rising costs are forcing many households to reduce retirement contributions because they need immediate cash for current expenses.

Older Americans nearing retirement are especially concerned about whether their savings will last long enough. Inflation and healthcare costs are creating fears that retirement funds may not provide long-term security.

Some Americans are delaying retirement completely because they cannot afford to stop working. Others are returning to work part-time after retirement to help cover living expenses.

Financial experts warn that middle-class Americans are increasingly vulnerable to retirement insecurity because many households have limited savings and growing debt obligations.

The retirement challenge is becoming even more serious as life expectancy increases and healthcare expenses continue climbing.

Economic Uncertainty Is Fueling Financial Anxiety

Economic uncertainty remains a major factor affecting middle-class confidence in 2026. Americans are increasingly worried about inflation, job stability, debt, and future living costs.

Consumer confidence has weakened in many areas as families become more cautious with spending. Many households are cutting back on vacations, restaurant visits, entertainment, and luxury purchases.

At the same time, Americans are becoming more focused on budgeting and financial planning. Families are tracking spending more carefully and searching for ways to reduce monthly costs.

However, experts say budgeting alone cannot solve all financial problems when essential living costs continue rising across the economy.

Many middle-class workers feel they are doing everything correctly financially but still struggling to move forward.

Household Debt Continues to Rise Across America

Debt levels across the United States continue increasing in 2026, adding more pressure to middle-class households. Reports show overall household debt remains historically high as Americans rely more heavily on borrowing.

Mortgage balances, credit card debt, auto loans, and student loans are all contributing to the growing financial burden carried by many families.

Financial analysts say rising debt levels become especially dangerous when combined with high interest rates and economic uncertainty. Households carrying large debt balances often struggle to build savings or invest for the future.

Lower-income and middle-income households are particularly vulnerable because they spend a larger portion of their income on necessities.

Americans Are Searching for Financial Stability

Despite growing financial pressure, many Americans are actively trying to regain control of their finances. Budgeting tools, debt reduction strategies, and financial education resources are becoming increasingly popular.

Financial advisors recommend several important strategies for middle-class households:

- Build emergency savings gradually

- Focus on paying down high-interest debt

- Reduce unnecessary monthly subscriptions

- Avoid impulse spending

- Create realistic financial goals

- Automate savings whenever possible

Experts also encourage families to prioritize long-term financial stability rather than lifestyle inflation or unnecessary borrowing.

However, many Americans say financial discipline alone is not enough when housing, healthcare, and everyday expenses continue climbing.

The Middle-Class Struggle May Continue Beyond 2026

Economic experts believe financial pressure on middle-class households could continue for years unless wages rise significantly and living costs stabilize.

Millions of Americans are working hard, paying bills, and trying to save, yet still feeling financially insecure. Rising debt, housing costs, inflation, and economic uncertainty are reshaping the financial reality of the American middle class.

For many households, financial stress is no longer temporary. It has become part of daily life.

As Americans continue adapting to economic challenges, the ability to budget carefully, avoid unnecessary debt, and build even small savings may become more important than ever before.